Award-winning PDF software

What is 2106-EZ Form: What You Should Know

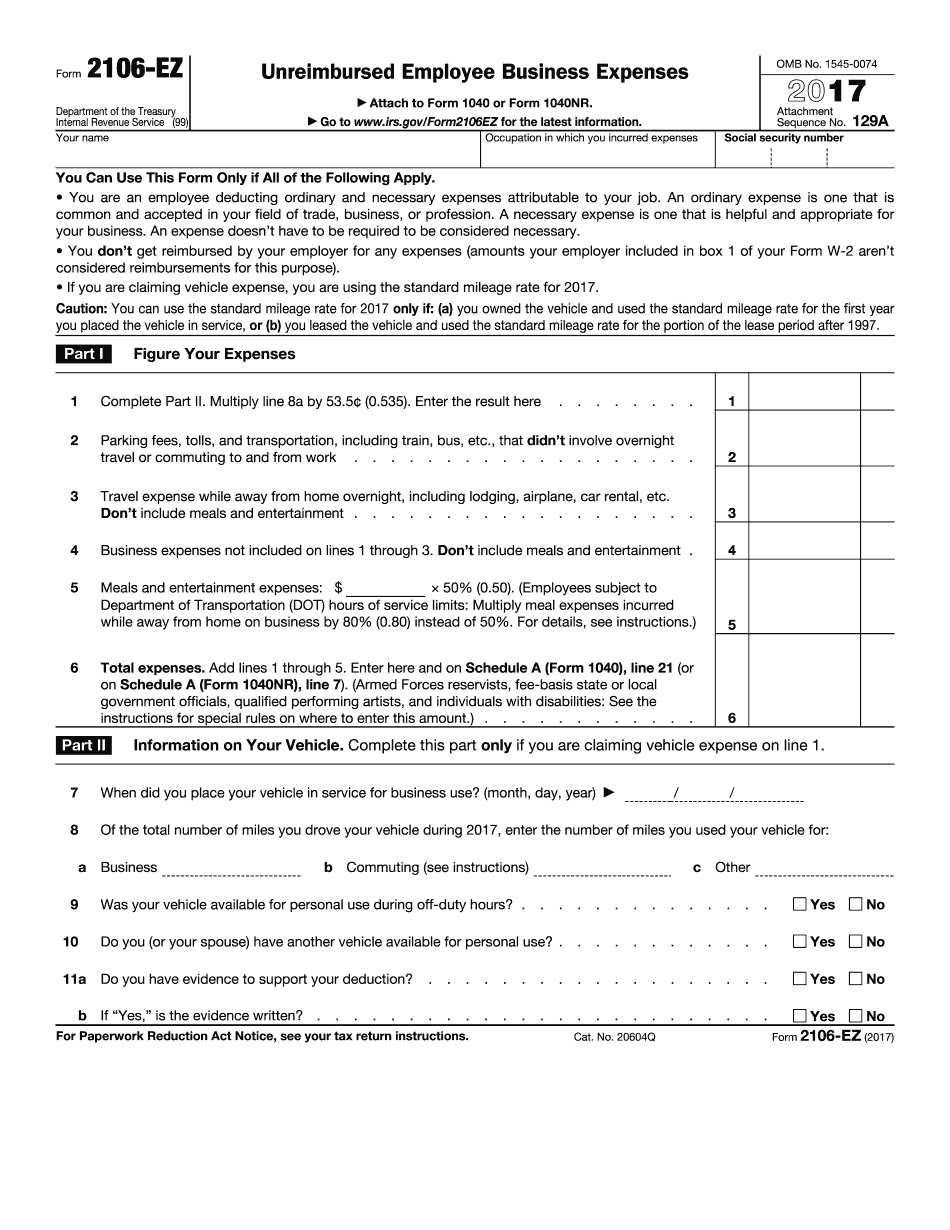

How to Use IRS Form 2106 for Non-Reported Expenses — TurboT ax Nov 13, 2025 — To use Form 2106-EZ as a non-reimbursed business expense deduction, you must use the same itemized deductions for work-related expenses that you itemize for regular business expenses. The only deductible expenses that you must use the itemized deductions for When you need to use IRS 2106, use Form 2106-EZ and Form 2106-J. You just need to keep track of your tax credits, so don't worry about that How to Use IRS 2106-EZ to Deduct Expenses for Self-Employed Individuals — TurboT ax Dec 23, 2025 — Use IRS Form 2106-EZ as self-employed business expenses deduction to save on tax credits, when the same itemized deduction you use to self-report regular business expenses. When you are using IRS itemized expenses for self-employment, you must report both itemized deductions and nontaxable expenses on separate forms. IRS 2106-EZ (2017) helps you remember to keep track of your tax credits, so don't worry about that. Do You Need to File a Statement With Your Itemized Expenses? — TurboT ax Sep 18, 2025 — Your itemized deductions for work-related expenses should be reported on IRS Form 2106-EZ. If you are self-employed, you can exclude the amount of itemized deductions on Schedule C, then use this form to report income and self-employment expenses to the IRS Include itemized deductions on Schedule C of your Form 1040.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 2106-EZ, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 2106-EZ online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 2106-EZ by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 2106-EZ from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.