Award-winning PDF software

Irs 2106 Ez Form: What You Should Know

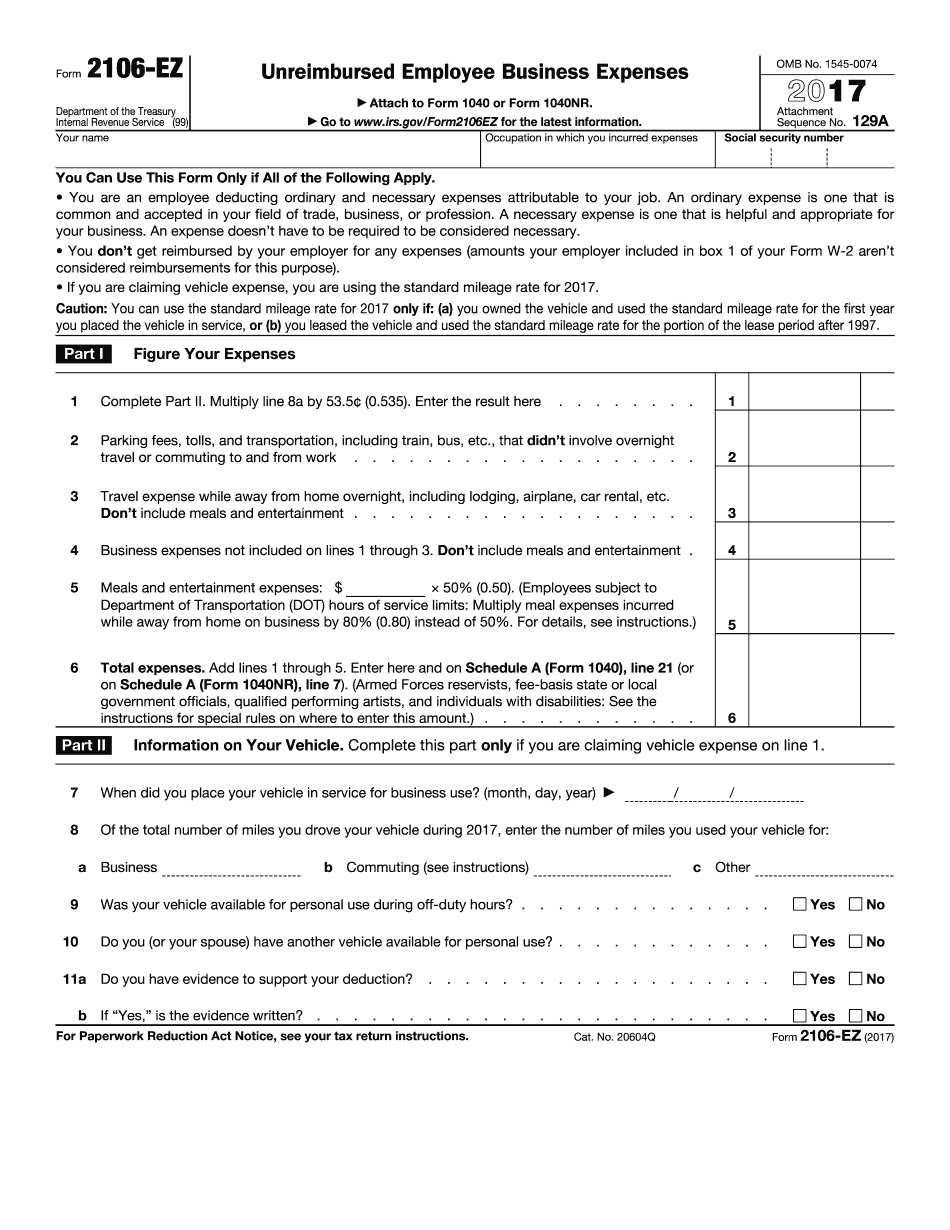

The first form to choose (or have the IRS send to you) is Form 2106, Employee Business Expenses (see below). The second form to choose (or have the IRS send to you) is the 2106-EZ, Employee Expenses For Business Use. Both forms can be used at the same time. What if I'm not an employee? The 2106-EZ is for use for employee business expenses (for example, a business expense for a personal property). An employee is an individual who has a regular and continuous workweek, who is actively involved in your business, and who does not earn income from their employment. The 2106-EZ is not available for the purchase, leasing, or sale of personal property. (For more information about the definition of an “individual”, see IRS Publication 926.) I use part of my own earnings to pay for my own business expenses. Should I use the 2106-EZ or the 2106? Generally, the 2106-EZ is used when the business owner or operator does not deduct an allowable deduction for ordinary and necessary business expenses that are related directly to the individual's profession or business (i.e., an expense is not deducted for interest, advertising, insurance, or professional services). If the business owner or operator deducts some or all of his allowable deductions based on the business owner's earnings, consider instead using the 2106-EZ. If I claim my business expenses as an employee on line 2 of my 2025 tax return, am I allowed to claim those expenses as business expenses using IRS Form 2106? Yes, you are authorized to claim that amount of allowable deductions. To see if you are entitled to claim this amount of deductions, go to for a table providing information on your tax year. In 2016, the IRS revised its standard operating procedures for claiming an adjustment for excess deductions claimed on line 2, and you may find this article helpful. What if I earn income that does not qualify as a business expenditure? What if I've already paid the applicable tax on my personal business expenses? If you are an employee, the IRS has rules that allow you to take an advance tax credit, known as Schedule C (Individual), to reduce the amount of taxes due. The IRS also has rules that allow you to take a non-itemized deduction for your personal business expenses, such as rent payments.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 2106-EZ, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 2106-EZ online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 2106-EZ by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 2106-EZ from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.