The Form 3800 forms, by contrast, allow an employer to report the cost of

The form is also used to report expenses that do not constitute the provision of services as an employee. These are the same expenses that are reported on Form 3800. The employee business expenses, in other words, are what you pay for services. The Form 3800 forms, by contrast, allow an employer to report the cost of goods and services provided to an employee for his or her services and to provide the employee with a summary accounting of the costs incurred, but these forms are generally not intended to enable an employer to report the cost of business-related business expenses of his or her employees. This information will be helpful if you are being audited. However, if you are only reporting the expenses incurred by your employees in providing your services as an employee, you may not need the Form 3800 at all. See Reportable business expense, later, to find out you cannot report business-related business expenses of employees of companies that do not deal with your trade or business. Employee Business Expenses (2106, Schedule1) Itemized Form 2106, Employee Business Expenses (2106, Schedule1) Itemized Form 3800 Expenses: (a) The employee-specific business costs on part I may include the following items in addition to any amounts included in Part I and paid with wages: (1) All food and nonfood items needed to serve food to the employee. (2) Nonfood items needed for cleaning and dressing purposes. (3) Nonfood items needed for personal and toiletry cleaning and drying. (4).

Filing a Faxed Return or Paper Return The following are specific requirements

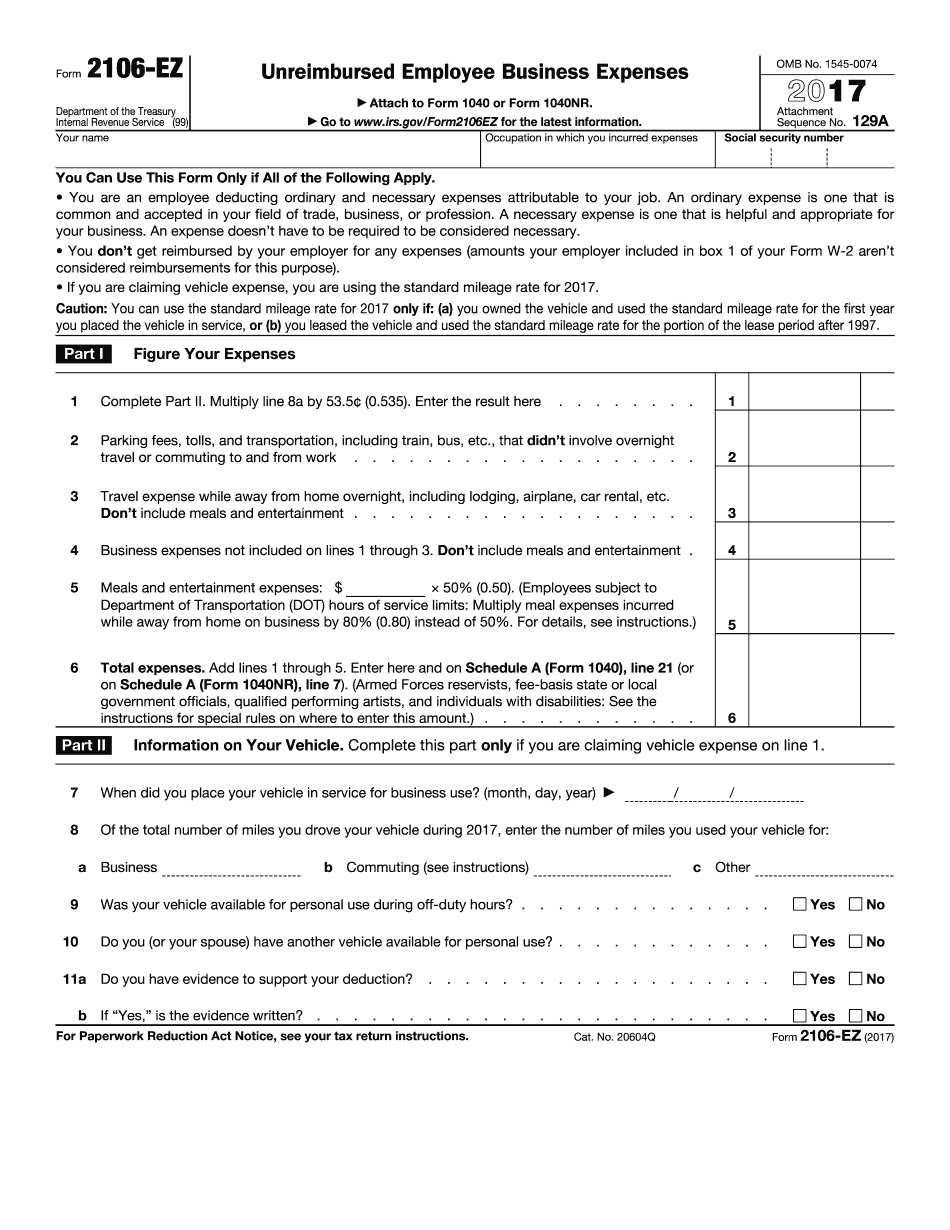

The following are specific requirements: Form 2106-EZ can be used for the following tax years: (2018 through 2025) Individual Income Tax Individual Income Tax Return Form 2106-EZ must be completed and returned to the proper address in this year. Filing a Faxed Return or Paper Return The following are specific requirements for filing a faxed or mailed return: Form 2106-EZ must be completed at the mailing address on the return You must send Form 2106-EZ by fax for federal return only using the IRS Network to ensure that all required information is received in timely fashion with no undue delay. For more information on electronic filing, visit the IRS Tax Tips for Small Businesses or call. Tax Year 2018 Form 5498-Ez Paper Return for Taxpayer Form 5498-Ez Paper Return for Taxpayer 2017 Additional information pertaining to the IRS Taxpayer Service Centers can be found on the IRS Website at.

If your total business income does not exceed 50 percent of your total

On September 31, 2016, the IRS released the 2016 Form 2106 for reporting deductible business expenses and the 2016 instructions for the Form 2106. Deductible Business Expenses for 2016 In 2016, you may not deduct all of your business expenses. Instead, you can deduct up to 50 percent of your total business income. You may use the following chart to determine if your total business income is more than 50 percent of your total business expenses under the 50 percent limitation. This determination can be done at both the time you file your income tax return and when you complete the 2016 Form 2106. If your total business income does not exceed 50 percent of your total expenses under the 50 percent rule, you don't have to enter in box 1 of Form 2106 your estimate of expenses you've incurred in the first tax year of your service. You then may deduct 50 percent of your expenses for the remainder of the year. You must include any allowable expenses in your income when determining your eligibility for the 50,000 limit. Furthermore, you must follow the same process with all expenses and expenses paid with contributions or services that you received in the first tax year that you serve. Furthermore, you must use the Form 2106 to report how much you spent at each place of business for business expenses incurred during the prior year. Furthermore, you need to complete one Form 2106 for each place that you operate. If you are married and file a joint return for your self-employed.

Results For Additional Information Contact the IU Bloomington Public Library at

Results For Additional Information Contact the IU Bloomington Public Library at 312.348.9243; or call Indiana University Public Library at.

Pension & Health Savings Accounts (HSA): Employees must participate in

Expense reimbursement: Expense reimbursement from HRB does not automatically include reimbursable expenses. Reimbursement may require a written request (e.g., H&R Block) through the Financial Management Service (FMS). For more information, you can access Expense Reimbursement. Pension & Health Savings Accounts (HSA): Employees must participate in qualified health savings accounts (HSA) at least once during each calendar year and at least once in each 12-month period for purposes of employer-paid health insurance benefits. To qualify for an HSA contribution toward an HSA account, employee or former employee must contribute at least 10 percent for the employee's own health insurance and at least 2 percent for the spouse's/dependent's health insurance, and, if self-employed, the employer must contribute. For more information regarding the contributions and coverage requirements, contact the CVS Healthcare Plan Administrator. Incorrect or Missing information? If you know any incorrect or missing information, please call our Information Center for a prompt response. If you need to report a change in address to H&R Block or a change in telephone number using a credit card, you may do so online, by mail or in person at a CVS store. H&R Block: Online: Mail: Corporate Address — CVS Pharmacy PO Box 2000 Baton Rouge, LA 70802 Phone: Fax: E-mail: corporatecvspharmacy.com Hours are Tuesday-Saturday 8 a.m.-4 p.m. Online: Mail:Corporate Address — CVS Pharmacy PO Box.

Award-winning PDF software