Award-winning PDF software

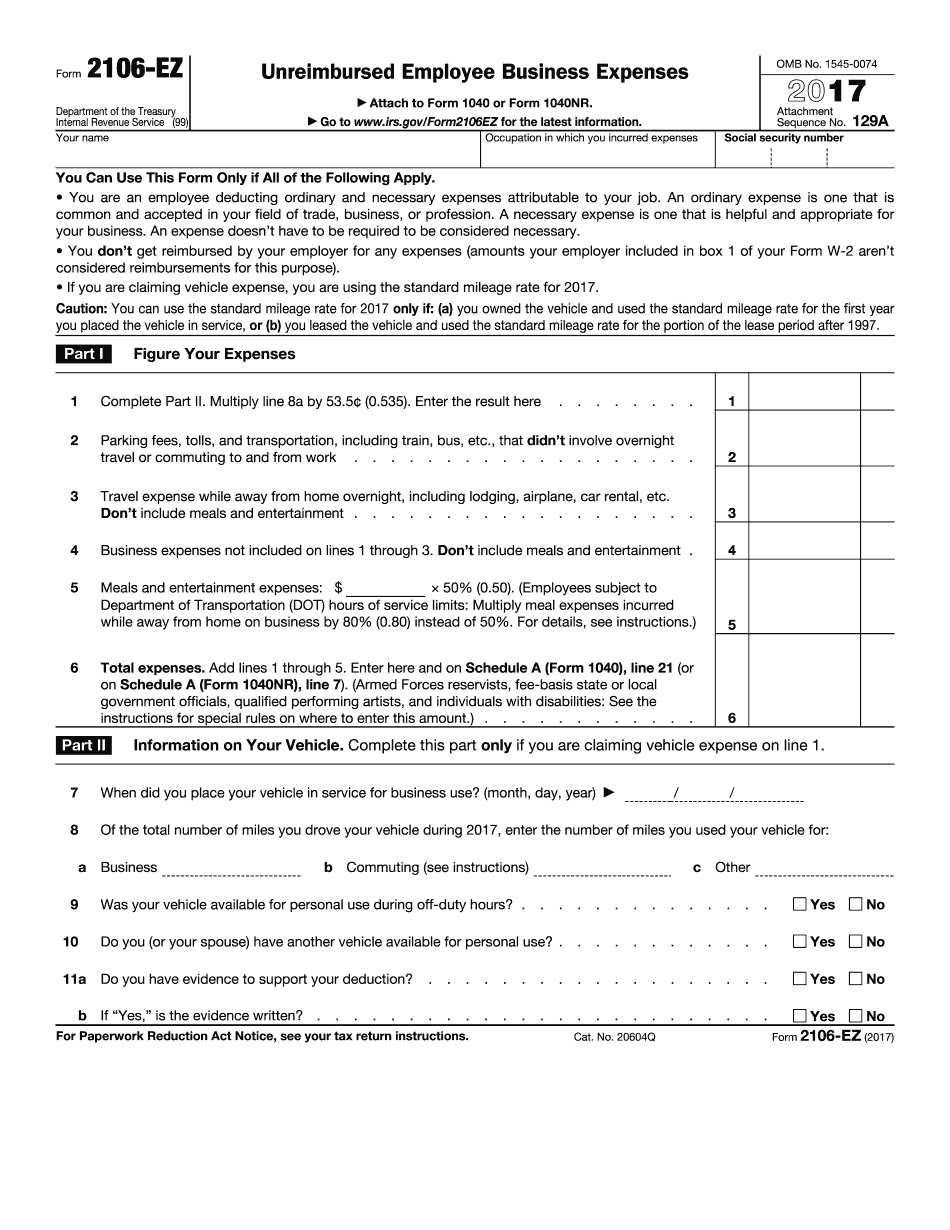

Santa Ana California Form 2106-EZ: What You Should Know

Rev. May 2017) Deputy Commissioner for Services and Enforcement. — Govini In a subsequent series of rulings, as well as an application to the Tax Court of New York. The Internal Revenue Service has granted an exception to this general rule and to the requirements of section 343(g) of the tax code by exempting from gross income from all transactions with a U.S. partner, the gross income of the U.S. general partner, a corporation, a partnership, or a trust other than a qualified trust, from a U.S. general partner to which section 7874 applies, and the gross income to a related person of a partnership (as defined in section 7872) from any other U.S. partner, the gross income from those transactions. (Rev. May 2017) In the case of a partnership, income allocated to the partnership which exceeds the amount allocated to each partnership partner would generally be treated as an overpayment as discussed in paragraphs (b) and (c) of this section. However, the partnership may exclude the excess from gross income under section 7704 or 7705 of the Internal Revenue Code. (Rev. May 2017) OMB No. Notice: Notice of proposed rule making and proposed regulations were published in The Federal Register on July 11, 2017. This was to receive public comment on specific items of proposed or final guidance. The comments must be addressed to the Commissioner of Internal Revenue, Federal Trade Commission, 1111 Constitution Avenue, N.W., Washington, D.C. 20580. (Rev. April 2017) Notice of proposal for rules: Notice of proposed rule making to amend Section 2.11.2 of the Internal Revenue Code (and make technical and conforming changes where necessary), and the proposed definitions of “covered financial entity” and “financial institution” in the section 2.11 of the Code as added by this notice, was published in The Federal Register on June 5, 2017. The comments must be addressed to the Commissioner of Internal Revenue, Federal Trade Commission, 1111 Constitution Avenue, N.W., Washington, D.C. 20580. (Rev.

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Santa Ana California Form 2106-EZ, keep away from glitches and furnish it inside a timely method:

How to complete a Santa Ana California Form 2106-EZ?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Santa Ana California Form 2106-EZ aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Santa Ana California Form 2106-EZ from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.